Charitable Trust Planning & Design.

A financial strategy with a charitable outcome.

Feasibility, structuring, and modeling for charitable remainder and lead trusts. We help design the trust - the payout, the term, the funding asset, the numbers - before it's ever signed, so the donor and their advisors can see exactly how it works.

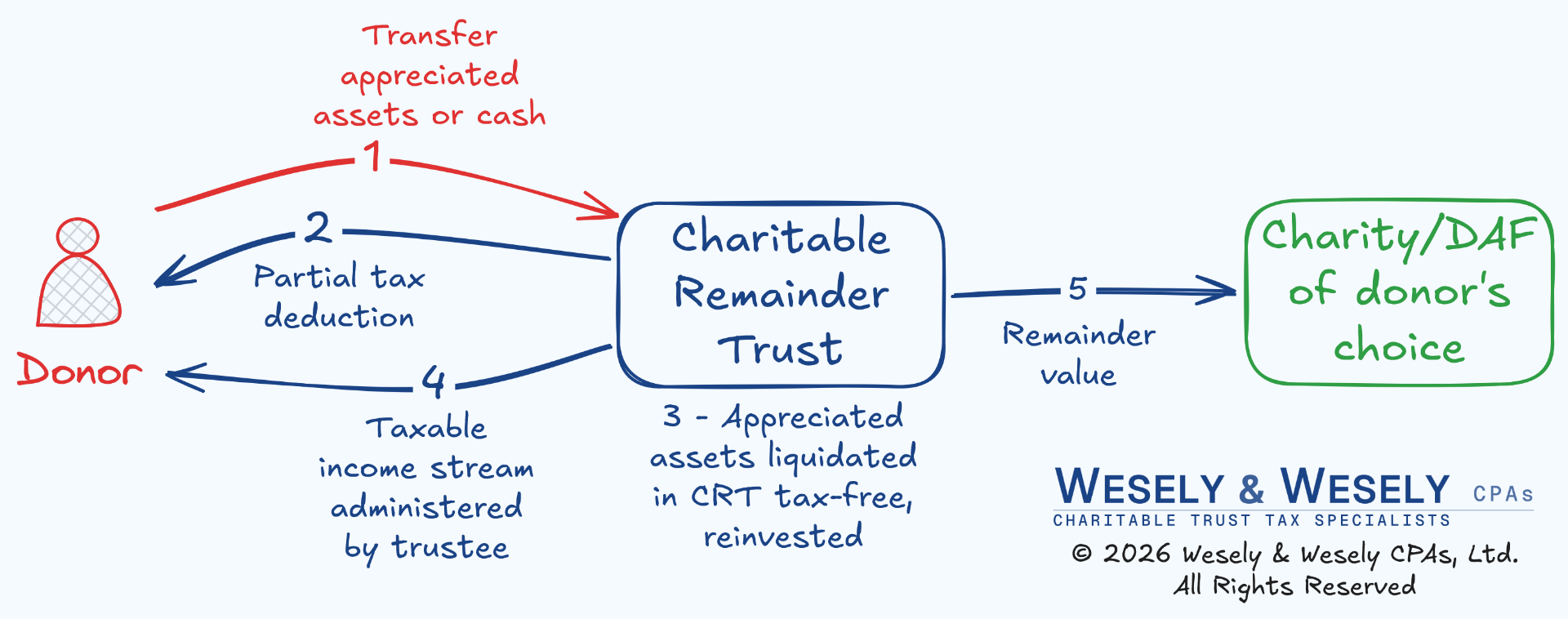

The basic shape.

- The donor transfers an appreciated asset into the trust.

- The donor takes a partial tax deduction in the year of the gift.

- The trust sells the asset with no immediate capital-gains tax.

- The donor (or a chosen beneficiary) receives an income stream for life or a set term.

- Whatever remains at the end goes to the donor's chosen charities.

This is the basic shape we design around.

When a CRT fits - and when it doesn't.

A CRT is worth modeling when:

- The core. The donor is comfortable giving up access to the principal in exchange for the tax-free sale of a donated asset and an income stream. That usually rests on two things:

- A large, appreciated "hot asset" - an asset with both a large built-in gain and an impetus to liquidate

- A desire for an income stream

- A significant charitable tax deduction would be valuable

- A desire to give to charity

- An estate large enough that reducing it matters

- A wish to shield assets from future creditors

Consider something simpler:

- A donor-advised fund - if there's no interest in an income stream, the donor wants to make a charitable impact now, or the asset is small

- A charitable gift annuity - if the donor wants an annuity income stream and doesn't want control over the investments

- QCDs - if the donor wants to make a charitable impact now and/or reduce the tax impact of IRA required minimum distributions

- No trust at all - if the donor isn't comfortable giving up the principal

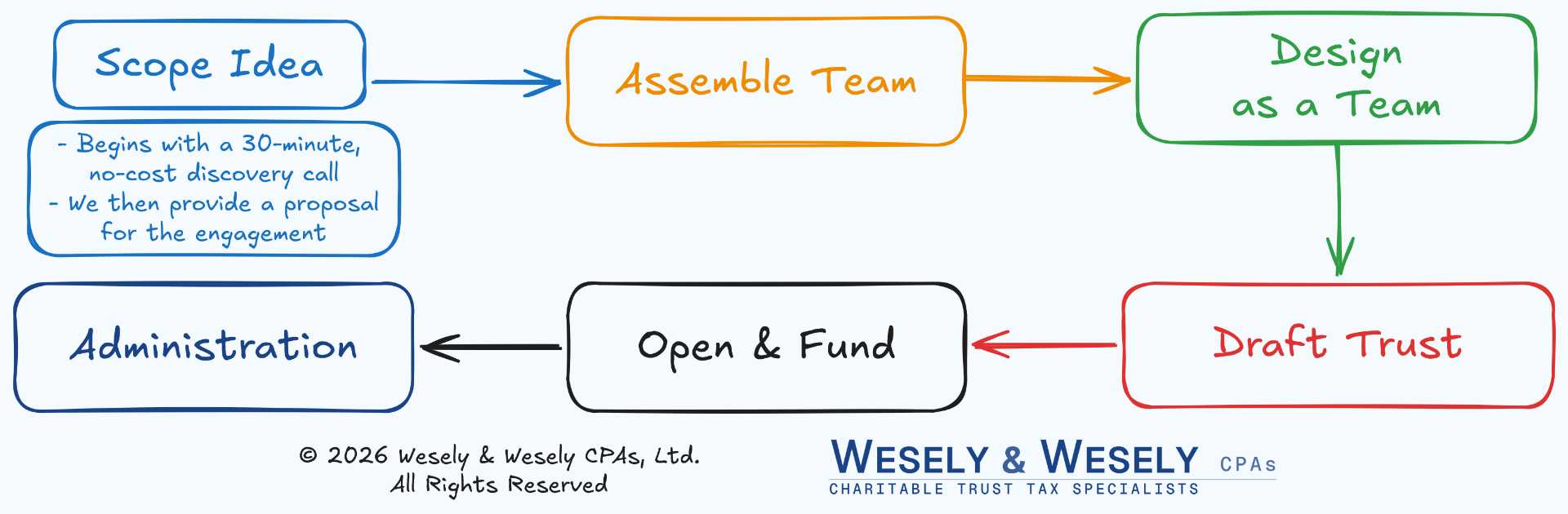

Forming a CRT, end to end.

The team doesn't change.

After the CRT is funded, the donor's existing team - financial advisor, attorney, and CPA - keeps doing exactly what it did before. None of those relationships need to change. We simply take the specialized trust filings off everyone's plate and make the annual rhythm as seamless as possible.

Charitable remainder trusts, in plain English.

01When does a charitable remainder trust actually make sense?+

A CRT tends to fit when someone has a large, appreciated asset they'd face a heavy tax bill to sell, they'd like an income stream from it, and they're comfortable giving up access to the principal in exchange for the tax savings and that income.

The charity that receives whatever's left is what makes the tax treatment work - but it doesn't have to be your reason for doing it. A lot of people come to a CRT as a financial move first, and the gift at the end is the outcome, not the starting point.

If any of that doesn't line up with your situation, a different tool is usually better - and we'll say so.

02CRT, donor-advised fund, or gift annuity - how do I choose?+

It comes down to whether you want an income stream, how much control you want over the assets, and the size of the assets involved. We model the options side by side with your real numbers so the choice is clear - and because we're CPAs, we can give you actual tax advice, not just lay the options out.

03How long does setting up a CRT take, and what will it cost?+

Most planning engagements run about two to six weeks, depending on the asset and how many advisors are at the table. We work on a fixed fee that we agree on up front, so there are no surprises - you'll know the number before we start.

04Do I have to change my financial advisor or attorney to do this?+

No. Your existing team keeps doing exactly what it did before. We handle the specialized trust piece and coordinate with everyone else - we're adding a specialist, not replacing the people you already trust.

What comes next.

Charitable Trust Tax Administration

Once the trust is funded, we handle the annual cycle - Form 5227, K-1s, unitrust calculations - and keep the existing advisor team intact.

Major Gift Consulting

Independent, vehicle-agnostic modeling for a specific gift - CRT, CLT, gift annuity, DAF, or outright.

Wondering whether a CRT fits your situation?

Start with a conversation. We'll model the options and tell you honestly whether a trust is the right tool - or point you to something simpler.