What a charitable remainder trust actually is.

In plain English, with a visual - because the idea is simpler than it sounds.

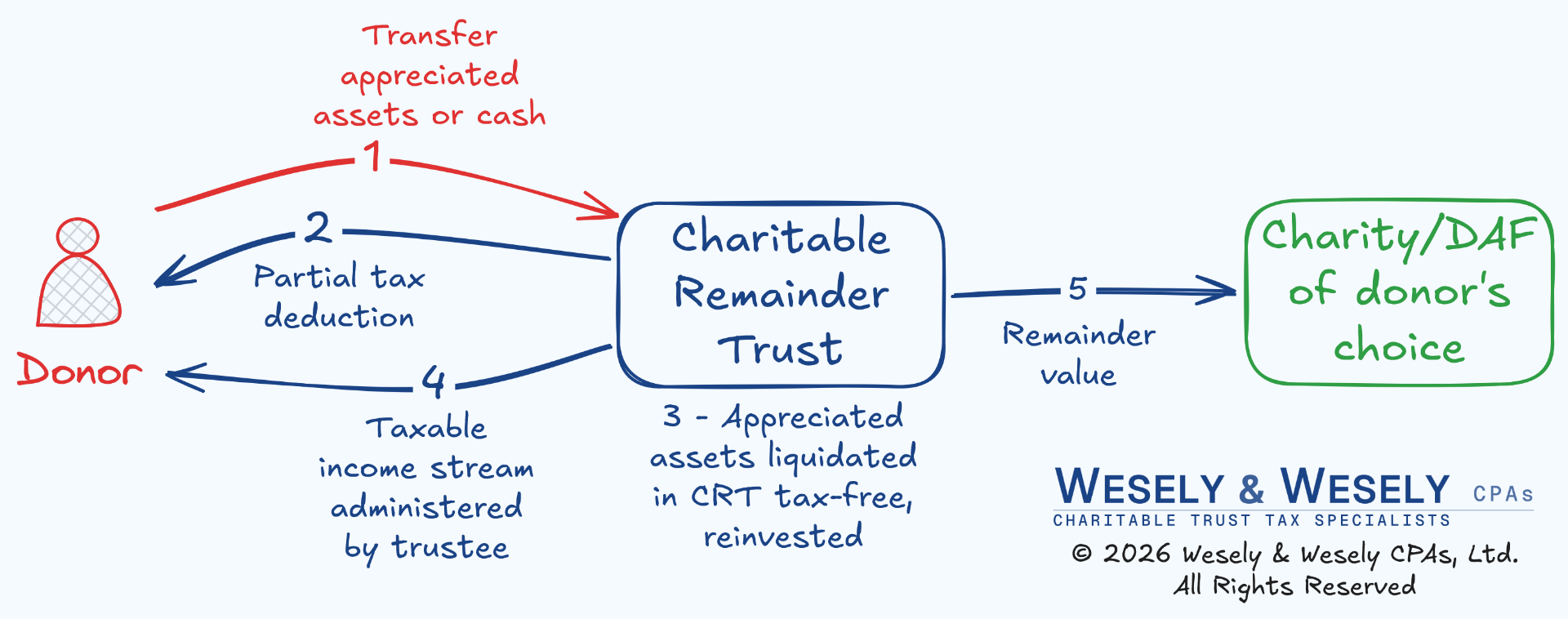

A charitable remainder trust gets explained in a lot of intimidating ways. Here's the honest, simple version.

Picture it as a flow:

- You give an appreciated asset - stock, real estate, farm assets, sometimes a business - into the trust.

- The trust sells it without the immediate capital-gains tax, so the full value stays invested and working.

- You get a tax deduction now, in the year of the gift.

- You receive an income stream - for life, or for a set number of years - generated off the full pre-tax value, not the smaller amount you'd have left after a taxable sale.

- Whatever's left at the end goes to a charity of your choosing.

That's the whole shape of it. Most people find it clicks the moment they see it drawn out, which is why we almost always start with a visual.

This is the kind of visual we'll draw with you - not a wall of tax code. If a trust isn't the right tool for your situation, we'll show you the simpler ones too.

You don't have to think of yourself as "charitable" for this to make sense

Plenty of people come to a CRT as a financial strategy first - a way to sell a concentrated asset without the tax hit and turn it into income. The gift at the end is the outcome, not a prerequisite. It's a financial strategy with a charitable outcome.

There's a real trade-off, and we'll be straight about it

You're giving up access to the principal in exchange for the tax savings and the income stream. For the right situation that trade is very much worth it - and for the wrong one, it isn't. If a simpler tool fits you better, like a donor-advised fund or a gift annuity, we'll tell you.

Wondering whether your situation is a fit? That's the first conversation we'd have - in plain English, no obligation.