Is a charitable trust right for me?

It comes down to one question, a few benefits that may or may not apply, and one real trade-off. Here's the whole thing in plain language - no jargon, no pressure.

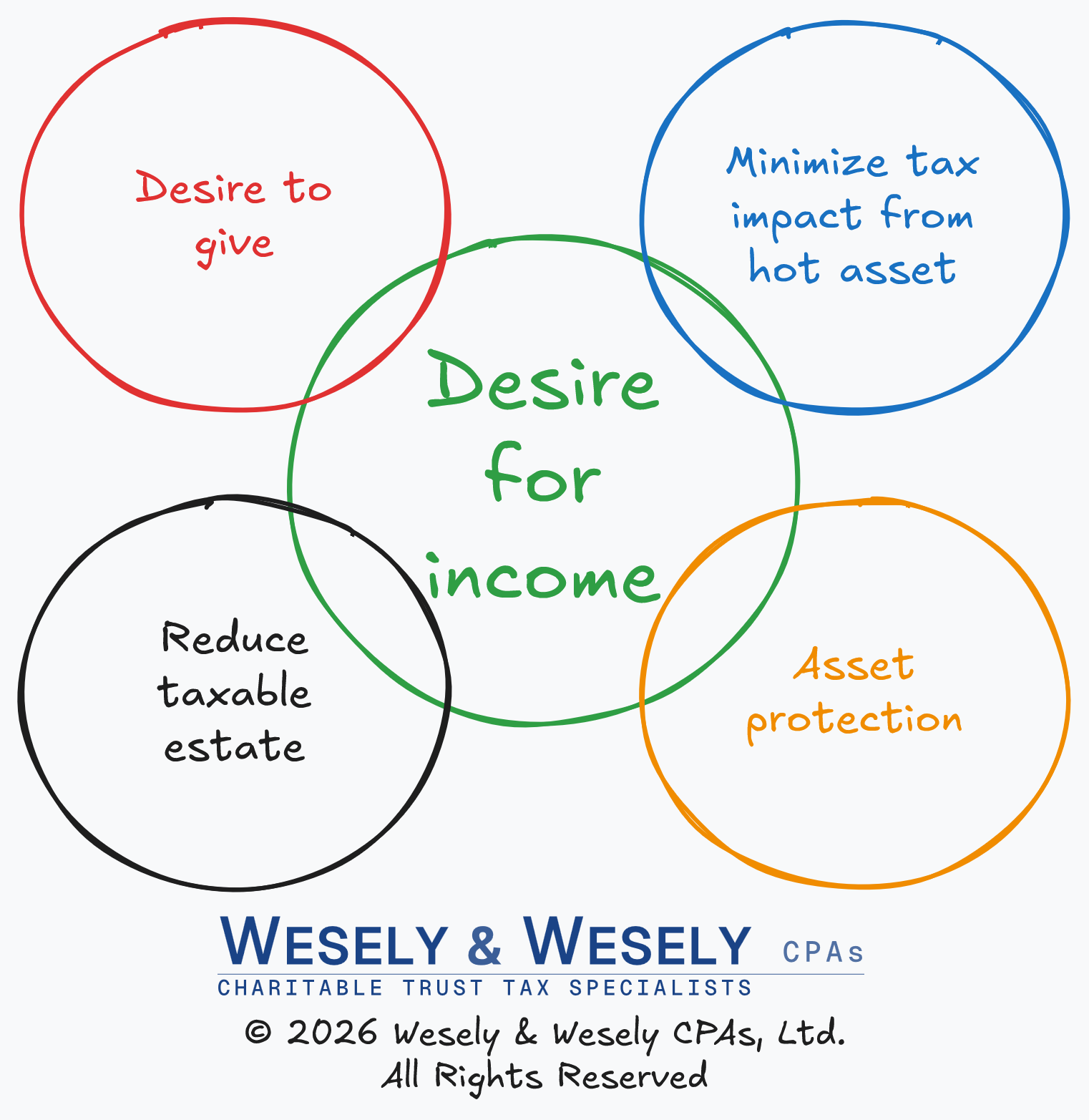

Most clients arrive with one or two of these motivations. A CRT becomes the right tool when several of them overlap at once. The tests below are how we check whether you're actually in that overlap.

This is the heart of it. A charitable remainder trust pays you - or someone you choose - income for life or a set number of years, and what's left at the end goes to the causes you care about. You don't have to need that income; a desire for it is the reason a CRT fits.

If a reliable income stream doesn't appeal to you, a CRT probably isn't the tool - and that's worth knowing early.

A donor-advised fund or an outright gift if you simply want to give, or a qualified charitable distribution from an IRA if you're over 70½. All accomplish the charitable goal without locking up principal.

You don't need all of them. Even one, alongside the income, can make a CRT worth modeling:

Minimizing tax on a “hot asset.” If you hold something with a large built-in gain - appreciated stock, real estate, a business interest - the trust can sell it without the immediate capital-gains tax. Helpful, but not required.

A desire to give. The remainder eventually goes to the causes you choose, so genuine charitable interest makes the arrangement more satisfying. Common - but, perhaps surprisingly, not strictly required.

Estate tax savings. Moving an asset into the trust can reduce what's exposed to estate tax, if your estate is large enough for that to matter.

Asset protection. Assets inside the trust are generally shielded from future creditors.

A CRT is irrevocable. Once you fund it, you give up access to the principal - and that's the reason behind most objections to a CRT. It's a fair concern. What you get in return is major tax savings and a reliable income stream.

Put simply: a CRT is a financial strategy with a charitable outcome. If giving up the principal feels like too much, that usually points toward a simpler, more flexible option - and we'll happily walk you through those.

If a reliable income stream appeals to you, one or more of those benefits fits, and you're comfortable giving up access to the principal - a charitable trust is worth modeling. If not, there's almost always a simpler path. Either way, the next step is a 30-minute conversation, not a decision.

Wondering which side of the tests you fall on?

Use the contact form. A sentence or two about your situation is enough; we'll respond within two business days with an honest take.